Charitable Gift Annuities: Strategic Income & Philanthropy in Tucson

A charitable gift annuity (CGA) is a sophisticated planning strategy that allows Tucson residents to make a meaningful contribution to a qualified nonprofit while securing a predictable, fixed income stream for life. At Global Investment Strategies, we serve as fiduciaries to ensure your giving aligns with your long-term wealth stewardship.

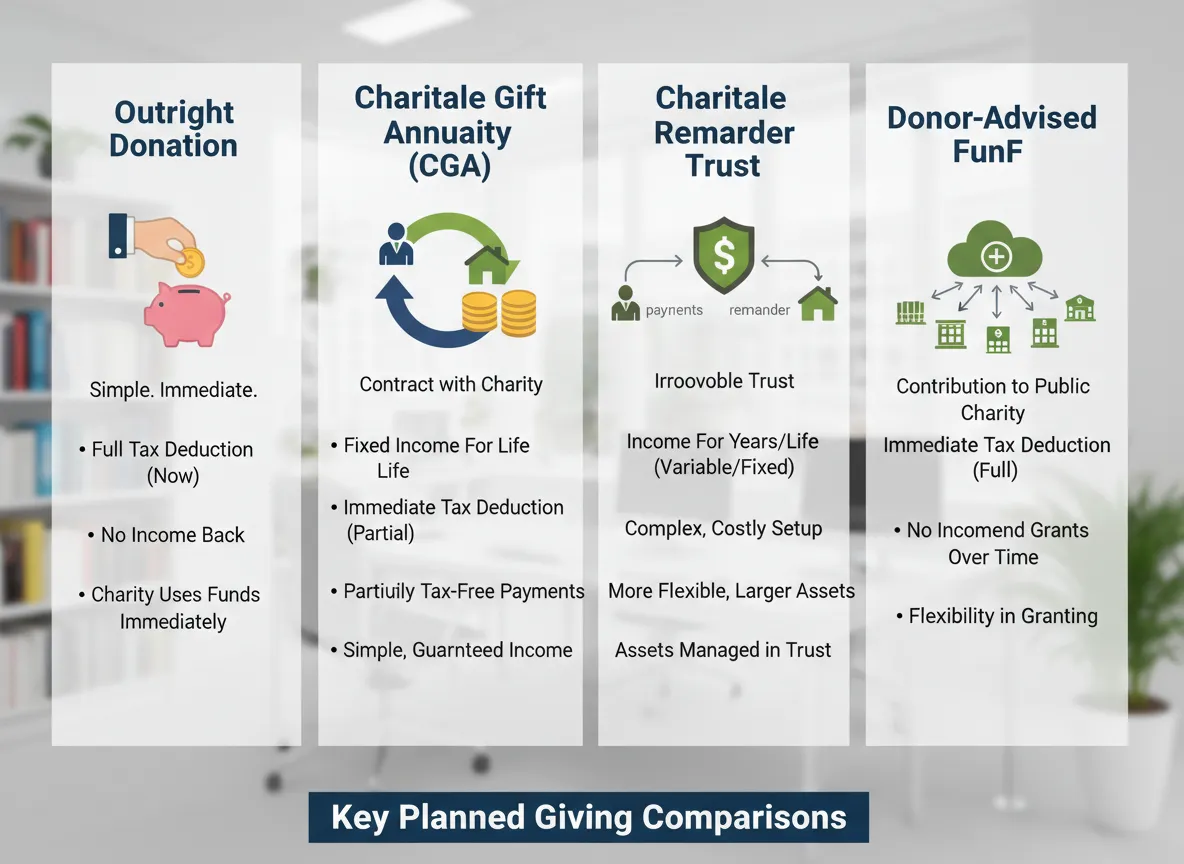

How CGAs Compare to Other Giving Strategies

| Estate Strategy | Benefit | Risk Addressed |

|---|---|---|

| Living Trust | Probate Avoidance | Public Record & Delay |

| Irrevocable Trust | Asset Protection | Estate Taxes / Creditors |

Who This Strategy Is Designed For

Individuals age 60 and older seeking predictable income

Charitably inclined donors who want to create lasting impact

Individuals with appreciated assets seeking tax efficiency

Those looking to reduce exposure to market volatility

Potential Advantages

Predictable income stream

Possible charitable income tax deduction

Potential capital gains tax advantages when using appreciated assets

Ability to support meaningful charitable organizations

Important Considerations and Limitations

CGAs are generally irrevocable once established

Fixed payments may not keep pace with inflation

Payments depend on the financial strength of the issuing charity

Not appropriate for individuals requiring short-term liquidity

Charitable Partnerships

Charitable gift annuities may be established with qualified organizations, allowing donors to align income planning with causes that support housing stability and community development.

Charity Financial Responsibility

Payments under a charitable gift annuity are obligations of the issuing charity and are not insured or guaranteed by the State of Arizona or any government agency. Donors should independently evaluate the financial strength of the charity.

Charitable gift annuities can be an effective strategy for individuals seeking to combine charitable giving with predictable income and tax-aware planning. Because CGAs are not suitable for every situation, careful evaluation and professional guidance are essential.

Important Arizona Disclosure:

Charitable gift annuities issued to Arizona residents are subject to Arizona law and oversight by the Arizona Attorney General’s Office. Payments are obligations of the issuing charity and are not insured or guaranteed by the State of Arizona. This material is for educational purposes only and does not constitute tax, legal, or investment advice. Arizona tax treatment may differ from federal tax treatment. Donors should consult their own qualified tax advisors regarding income, capital gains, and estate tax implications.

Insurance planning may help protect the income plan from risks that could affect family continuity, business succession, estate liquidity, or long-term support needs.

Permanent life insurance, buy-sell insurance, key-person coverage, and certain cash-value strategies should not be evaluated in isolation. They should be reviewed in the context of the client’s income needs, tax picture, estate plan, business structure, and risk profile.

The SEC encourages investors to understand annuity costs, surrender charges, tax treatment, and suitability before buying annuity products, particularly because annuities are generally long-term vehicles and can involve fees, tax consequences, and investment or insurer risk depending on the product type (SEC Investor Bulletin on Variable Annuities).

The Core Components of a Strong Income Plan

A strong income plan should be comprehensive. It should not rely on a single product, one account, or one rule of thumb.

Cash Flow and Lifestyle Needs

The first question is practical: What income is needed, when is it needed, and for what purpose?

This includes lifestyle spending, taxes, healthcare, debt obligations, charitable giving, family support, business commitments, insurance premiums, and estate planning needs.

Tax-Aware Distribution

The second question is tax-aware: Which income sources should be used, and in what order?

Income planning may involve taxable accounts, tax-deferred accounts, Roth accounts, annuity payments, charitable tools, business distributions, sale proceeds, or insurance strategies. Each may have different tax implications.

Retirement Income

Retirement income is still a major part of income planning. A retirement income plan may include Social Security, pensions, retirement accounts, annuities, investment income, cash reserves, and withdrawal strategies.

The key point is that retirement income is one part of income planning, not the entire category.

Business-Owner Income

For business owners, income planning should address how business cash flow, ownership value, succession planning, ESOP structures, insurance, and exit proceeds may support the owner’s personal financial future.

This is where income planning connects directly to business planning.

Charitable Income Planning

Charitable income planning may include charitable gift annuities, charitable remainder trusts, qualified charitable distributions, donor-advised funds, beneficiary designations, or other strategies reviewed with qualified professionals.

The purpose is not simply to give assets away. The purpose is to coordinate generosity with income, tax awareness, estate planning, and legacy impact.

Estate and Legacy Coordination

Income planning should be reviewed alongside estate planning. The assets used for income today may affect what is available for heirs, charities, trusts, taxes, or estate liquidity later.

Estate planning can help clarify where assets should go. Income planning helps determine how assets are used along the way.

Insurance and Risk Protection

Insurance planning may support income planning by protecting against premature death, business disruption, estate liquidity needs, long-term obligations, or succession risk.

Insurance is not the income plan by itself. It is one possible planning vehicle that may support or protect the income plan.

The GIS Income Planning Framework

GIS presents income planning as a coordinated framework built around four questions.

What Income Do You Need?

This includes lifestyle, taxes, healthcare, family support, charitable commitments, business obligations, and legacy goals.

Where Will Income Come From?

Potential sources may include portfolio withdrawals, Social Security, pensions, annuities, business income, business-sale proceeds, ESOP-related liquidity, charitable income tools, insurance policy values, rental income, or other assets.

How Should Income Be Protected?

The plan should consider taxes, inflation, market volatility, sequence-of-returns risk, healthcare risk, business risk, liquidity risk, and family continuity risk.

What Should Income Accomplish?

Income should not only fund spending. It may also support independence, family security, charitable impact, business continuity, estate liquidity, and legacy stewardship.

Planning Vehicles That May Support Income Planning

Income planning is the parent conversation. The planning vehicles below may help solve different parts of the income planning problem.

Estate Planning

Estate Planning helps connect income decisions with family continuity, beneficiary planning, trust funding, insurance strategies, charitable goals, and legacy intent.

Income planning should connect to estate planning because income decisions can affect what remains for heirs, how assets pass, how taxes are handled, and whether the client’s financial life supports the intent of estate documents.

Business Planning

Business Planning helps business owners move from active operator to steward. It connects income planning with succession, exit planning, buy-sell coordination, executive retention, key-person risk, and building personal wealth beyond the company.

Income planning should connect to business planning because many business owners need to convert business value into personal income and family financial security.

Retirement Planning

Retirement Planning is a major subset of income planning. It focuses on the transition from paycheck to portfolio and the need to manage taxes, inflation, healthcare costs, market timing, and portfolio income.

Income planning should connect to retirement planning because retirement is often the moment when income planning becomes urgent.

Charitable Gift Annuities

Charitable Gift Annuities may be relevant for charitably inclined clients who want to support a qualified organization while receiving fixed lifetime payments.

Income planning should connect to charitable gift annuities because charitable income tools can help connect income, tax awareness, generosity, and legacy planning.

Income For Life

Income For Life supports the transition from accumulator to steward by focusing on dependable lifetime income strategies and the psychological shift from building assets to using assets with purpose.

Income planning should connect to Income For Life because lifetime income is one of the most important outcomes some clients want from a broader income planning process.

ESOP Structures

ESOP Structures may help business owners, founders, and employee-owned companies understand the risks and planning considerations around employee ownership, repurchase obligations, buy-sell funding, key-person protection, and Section 1042-related planning.

Income planning should connect to ESOP structures because ESOP planning can affect owner liquidity, employee retirement benefits, business continuity, and the owner’s personal income plan.

Insurance

Insurance can support income planning when it is coordinated with estate planning, business succession, liquidity needs, supplemental retirement considerations, or legacy goals.

Income planning should connect to insurance because insurance may protect the plan from risks that could disrupt income, family continuity, or business succession.

Income Planning Vehicle Matrix

| Planning Vehicle | What It Helps Solve | How It Supports Income Planning |

|---|---|---|

| Estate Planning | Family continuity, beneficiary alignment, estate liquidity, legacy intent | Helps ensure income decisions do not conflict with long-term transfer goals |

| Business Planning | Owner transition, succession, buy-sell funding, business liquidity | Helps business value become personal income and family security |

| Retirement Planning | Portfolio withdrawals, Social Security, healthcare, tax timing | Helps accumulated assets support retirement lifestyle |

| Charitable Gift Annuities | Charitable intent plus fixed lifetime payments | Connects giving with income and legacy goals |

| Income For Life | Lifetime income confidence and accumulator-to-steward transition | Helps create dependable income strategies for long-term planning |

| ESOP Structures | Employee ownership, repurchase liability, owner liquidity, succession | Connects ESOP planning with personal income and estate considerations |

| Insurance | Risk protection, estate liquidity, succession, supplemental planning | Helps protect income, family continuity, and legacy outcomes |

Questions to Ask Before Building an Income Plan

Before choosing any planning vehicle, clients should ask:

What income do I need for lifestyle, taxes, healthcare, family, and giving?

Which income sources are guaranteed, variable, taxable, tax-deferred, or tax-free?

What happens if markets decline early in the income phase?

How much of my wealth is tied to a business or illiquid asset?

How will required distributions affect my tax picture?

Are charitable goals part of the income plan?

Does my estate plan reflect how income will be used during life?

Is insurance needed to protect family, business, or estate objectives?

Which professionals should be involved before implementation?

Common Income Planning Mistakes

Treating Income Planning as Only Retirement Planning

Retirement planning is important, but it is not the full picture. Income planning should also consider tax strategy, business ownership, charitable planning, insurance, estate planning, and legacy goals.

Focusing on Gross Income Instead of Net Income

A strategy may appear attractive before taxes but produce a different result after taxes, fees, liquidity limits, or timing issues.

Ignoring Business-Owner Complexity

Business owners often need a different income planning process because income may depend on business cash flow, succession timing, buyer terms, ESOP structure, or key-person continuity.

Separating Charitable Planning From Income Planning

Charitable planning can affect income, taxes, estate planning, and legacy. It should be integrated into the full income plan when charitable intent exists.

Leaving Insurance Out of the Conversation

Insurance may not be needed in every case, but when family continuity, business succession, estate liquidity, or long-term obligations are present, insurance should be reviewed as part of the planning conversation.

Making Product Decisions Before Planning Decisions

Income planning should begin with goals, risks, cash flow, taxes, and coordination. Products and vehicles should come later.

Frequently Asked Questions

What is income planning?

Income planning is the process of coordinating assets, accounts, business interests, insurance strategies, charitable tools, and estate goals so they can support income needs and long-term planning objectives.

Is income planning the same as retirement planning?

No. Retirement planning is a major part of income planning, but income planning is broader. It can include tax-aware distribution, business-owner income, charitable income tools, estate planning, insurance, ESOP structures, and legacy planning.

Why is income planning important for business owners?

Business owners may have significant wealth tied to the company. Income planning helps coordinate business transition, owner liquidity, personal income, succession risk, estate planning, and insurance.

Can charitable giving be part of income planning?

Yes. For charitably inclined clients, charitable strategies may connect income, tax planning, and legacy goals. These strategies should be reviewed with qualified legal and tax professionals.

How does estate planning connect to income planning?

Describe the item or answer the question so that site visitors who are interested get more information. You can emphasize this text with bullets, italics or bold, and add links.

How does insurance connect to income planning?

Insurance may help protect income planning by addressing risks such as premature death, business disruption, estate liquidity needs, or succession obligations.

What is the first step in income planning?

The first step is to define income needs, identify income sources, understand tax and liquidity constraints, and review how income decisions connect to estate, business, charitable, and insurance goals.

Request a Private Income Planning Conversation

Income planning is not a single product decision. It is a coordination process.

If you are approaching retirement, transitioning a business, reviewing charitable income strategies, evaluating insurance, or trying to connect income with estate and legacy goals, Global Investment Strategies can help you move from complexity to clear thinking. 123

Sources and Further Reading

Move from Complexity to Clear Thinking

Important financial decisions deserve thoughtful review and experienced co-ordination. Request a private conversation to discuss your goals.

Global Investment Strategies provides educational planning concepts and works alongside your qualified legal, tax, and financial professionals. We serve the greater Tucson community, including Oro Valley, Catalina Foothills, Marana, and surrounding areas.| Copyright 2026. Global Investment Strategies. Tucson, Arizona. All Rights Reserved.