Retirement Plan Pivot: Rising Digital Healthcare Costs

For decades, traditional retirement planning has relied on a standard, passive assumption: if you peg a portfolio's distribution rate to a general consumer inflation index, your long-term purchasing power remains secure.

In the current economic landscape, that assumption is breaking down. This vulnerability is not driven by macro interest rate cycles, but by a fundamental, structural shift in how high-level medical care is delivered, packaged, and priced.

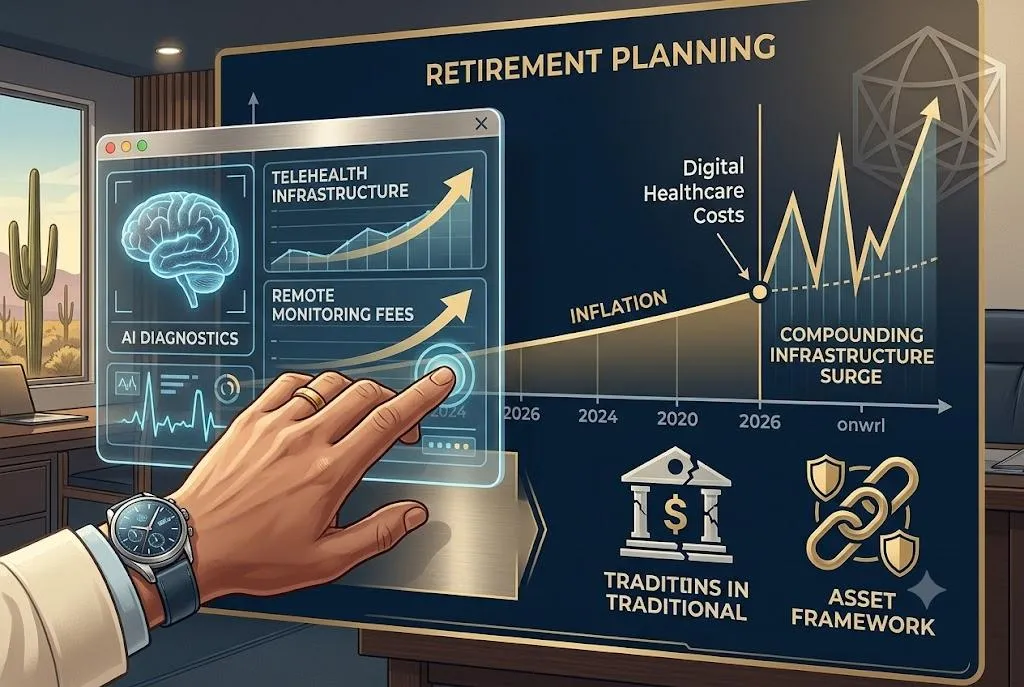

The integration of advanced AI-driven diagnostics, remote monitoring infrastructure, and private premium digital health platforms has introduced an entirely new category of localized cost acceleration. These are not standard, predictable medical bills; they are compounding infrastructure fees that traditional financial models completely fail to capture.

To protect long-term estate value and ensure smooth multi-generational transitions, sophisticated wealth coordination must pivot away from outdated, generic inflation rules and design frameworks built for technical reality.

Dismantling the General Inflation Myth

When preparing an estate for the distribution phase, evaluating future healthcare obligations through a broad Consumer Price Index (CPI) lens creates a significant blind spot. Advanced digital care—the exact tier of proactive, specialized medicine that business owners, executives, and families rely on to maintain their quality of life—is scaling at a trajectory completely disconnected from standard consumer goods like food or fuel.

If a retirement roadmap treats these specialized medical expenses as a fixed, flat line item adjusted by a generic 3% or 4% annually, the underlying capital is exposed to unexpected stress.

A disciplined strategy requires planning for structural volatility. When specialized regional medical centers implement premium technology surcharges or tier their digital access, those costs hit an estate sequentially, compounding year over year. Without dedicated, cross-disciplinary coordination, families are frequently forced to liquidate highly productive, tax-advantaged assets prematurely simply to cover short-term cash-flow gaps.

The Illiquidity Trap: The true risk to a wealth blueprint isn't just the dollar amount of a specialized invoice; it is the timing of the liquidation. If an estate lacks the deliberate structural liquidity to absorb a sudden surge in premium digital health fees during a broader market correction, the owner is forced to sell equities at a loss, permanently altering the lifetime trajectory and legacy of the portfolio.

Integrating Health Volatility into Estate Frameworks

Amending this vulnerability is not a matter of taking on more investment risk or chasing speculative returns; it is a matter of strict asset coordination. To insulate an estate against digital healthcare acceleration, the underlying capital must be structured to match the exact nature and timing of the liability.

Strategic Premium Financing: Aligning specific tax-advantaged vehicles to absorb the weight of premium health structures without disrupting the primary growth engine of the estate.

Contractual Cash-Flow Engineering: Deploying highly structured annuity frameworks specifically designed to yield predictable distributions that correlate with escalating fixed liabilities. By offsetting healthcare infrastructure costs with guaranteed structural income, the broader investment portfolio remains entirely free to focus on long-term capital appreciation and legacy goals.

Cross-Disciplinary Coordination: Ensuring that your estate planning documents, corporate business entities, and liquid portfolios are communicating seamlessly. Decisions regarding health preservation and longevity overhead should never be made in isolation from your overarching tax and legacy blueprints, a core tenet outlined by industry retirement risk frameworks.

The Bottom Line

A successful transition into retirement is never about guessing the future, reacting to economic noise, or relying on generic templates; it is about establishing a structure disciplined enough to withstand systemic shifts.

Digital advancements are fundamentally rewriting the economics of longevity. By addressing these tech-driven medical overhead costs through proactive structural design rather than retroactive, panicked portfolio withdrawals, Southern Arizona families can effectively eliminate unnecessary complexity, protect their core assets, and maximize the long-term value passed to the next generation.

Educational Notice

This material is strictly for educational purposes and should not be construed as financial, legal, or tax advice. Global Investment Strategies does not provide tax or legal opinions. For specific strategies tailored to your unique circumstances, consult with our professional team.